Hedging strategies: how to stay on the board without fear

Surfing the price wave for as long as possible – that is the goal of most investors. However, recent days have shown that markets are more vulnerable to setbacks, also due to high valuations. A suitable hedging strategy can reduce the risk of large losses without sacrificing potential price gains.

Text: Claude Hess

As of mid-November, the US S&P 500 Index climbed to an all-time-high valuation with a long-term price-earnings ratio1 (P/E ratio) of over 37. Even though the valuation has been somewhat reduced since then as a result of the new «Omicron» coronavirus variant, it is still at a very high level in a historical context. For comparison: in autumn 2007, before the S&P 500 Index collapsed as a result of the financial crisis, the long-term P/E ratio was only 23. The justification for the high equity valuation is often based on the following argument: since interest rates are at a very low level or even negative, equities still offer an attractive risk premium relative to bonds despite their high valuation. With the feared upward pressure on interest rates as a result of higher inflation, however, this argument is now threatening to lose its clout.

Protection of bonds put to the test

In the past, bond investors also enjoyed higher prices. Due to the long-term trend of falling interest rates, bonds were even the better investment compared to equities from a risk/return perspective. In addition, bond investors were not hit in times of falling share prices. For instance, the equity prices that fell during the financial crisis were partially offset by the increased bond prices. Bonds have served as the optimal diversifier in a mixed portfolio in past years as the correlation between equities and bonds has been negative in recent years. However, looking back at the further history shows that the negative correlation between equities and bonds is not a matter of course. Studies2 show that one of the main drivers of the increasing correlation between equities and bonds is inflation. For example, in the 1970s, which was a period of high inflation, the correlation between US equities and bonds was negative. The currently high latent inflation risks are a pointer against relying completely on the protective effect of bonds. Even though traditional multi-asset solutions can mitigate this risk to a certain degree through tactical management, the question arises about alternative hedging strategies to protect against falling equity markets.

Put options as an attractive hedge

One possibility is to hedge the equity risk of a portfolio with futures. This is equivalent to investing in the risk-free interest rate and would therefore no longer offer any participation in rising equity markets. However, market extremes can often last longer than expected, and a forecast of when a bubble bursts is associated with enormous uncertainties.

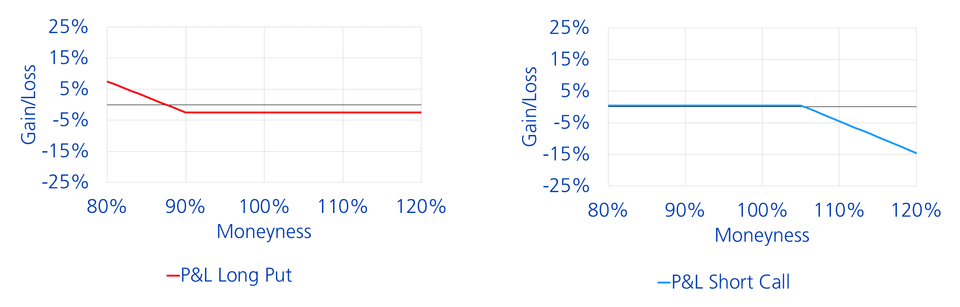

Another type of hedge is to purchase out-of-the-money put options on equity indices. This asymmetric hedging instrument hedges high losses, such as greater than ten percent. At the same time, the upside potential minus the option premium is maintained. Since the price of (put) options depends on market volatility, late-cycle market phases with low market volatility in particular represent an attractive market environment for the use of put options.

Permanent protection is better than market timing

One-off hedging with put options only offers temporary protection. If market slumps only occur after the option has expired, hedging does not provide any benefits. It is therefore advantageous to select an option strategy with a permanent hedging effect. As the hedging effect of a single put option gradually «fizzles out» with rising share prices, a staggered renewal of put options is also recommended. This way, the protective effect can be «refreshed» again after share prices have risen.

A collar for any eventuality

The tiered put options strategy protects against high losses, but comes at a cost. Costs can be attenuated if some of the upside potential on the equity markets is sacrificed. This is achieved by selling out-of-the-money call options. As a result, investors initially participate in the equity market development in the case of rising prices. Only once the prices exceed the strike price of the sold call option will participation stop3. An options strategy that combines the purchase of out-of-the-money put options with the sale of out-of-the-money call options is called a «collar strategy». This is because both the loss potential and the upside potential are limited.

Better risk/return ratio thanks to the collar strategy

The use of a collar hedging strategy is suitable for security-conscious investors who want to participate in late-cycle market phases but still want to be prepared for major setbacks on the equity markets. It is also suitable for those who believe that bonds have already had their best days as a hedging instrument in a multi-asset portfolio. The collar hedging strategy makes it possible to forego some bonds in the portfolio and invest in asset classes with better risk-return expectations. This can improve the expected return of a mixed portfolio in relation to the risk taken. In view of the relatively high hedging expenses, implementation – both for disposable assets and pension assets – can be carried out most efficiently within a multi-asset fund.

1 Equity index divided by the average inflation-adjusted earnings of the last ten years.

2 «Risk and return of different asset allocations», Norges Bank discussion note, 2016.

3 In this case, the buyer of the call option is compensated financially, i.e. no underlying asset needs to be delivered.