Equity prices & Interest rate sensitivities: A bottom-up perspective

Why are stock returns so sensitive to rising interest rates and how could investors better consider this risk in the investment decision-process? One way to answer this question is by looking at the equity market from a bottom-up perspective.

Text: Diego D'Argenio

After many years of double-digit returns, equity investors have become too complacent about market conditions and have clearly underestimated the potential re-pricing implication for equity markets due to a change in monetary conditions. Even though the Fed sent a clear signal at the December FOMC meeting about how serious it was in fighting rising inflation, equity markets did not react until recently this year.

Why are stock returns so sensitive to rising interest rates?

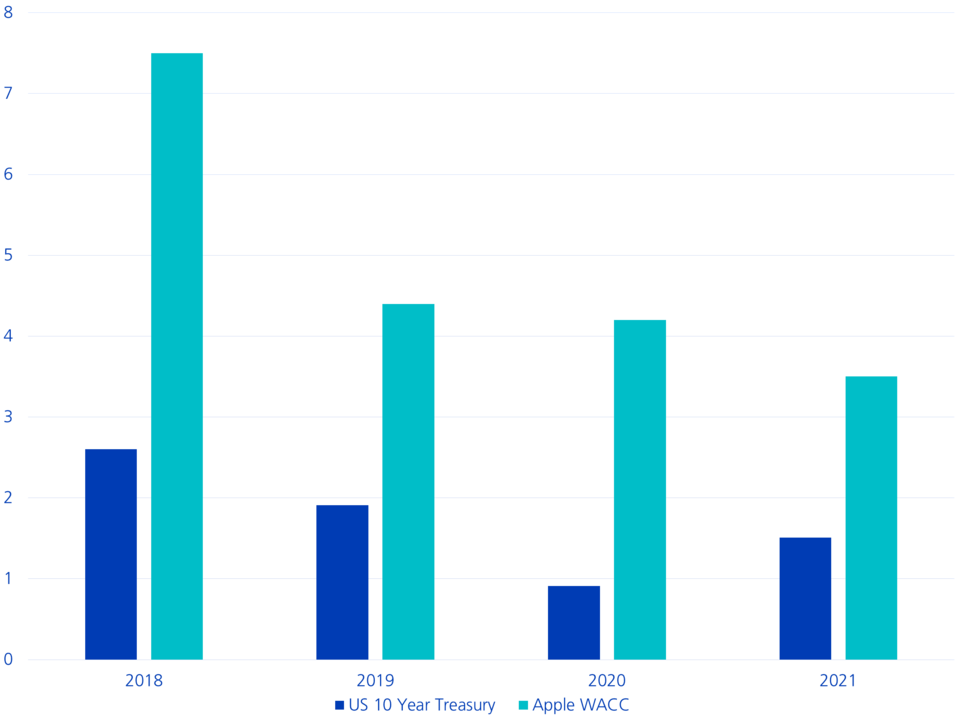

The interest-rate sensitivity is very much the reflection of the stock-valuation process. Let's consider an example by reviewing Apple financials data. From the table one can see that the fundamental financial performance of Apple was astonishing: the Return on Invested Capital (ROIC) over the past 3 years averaged 35% and the EPS almost doubled in only 2 years. On the back of this financial performance, which was accompanied by strong share price gains, the implied cost of capital of Apple declined from 7.5% to 3.5%:

| 2018 | 2019 | 2020 | 2021 | |

| ROIC | 22.8% | 24.7% | 28.1% | 46.1% |

| CFO | 77.4 | 69.3 | 80.6 | 104 |

| Capex | 12.4 | 10.4 | 7.3 | 11 |

| Div | 13.7 | 14.1 | 14 | 14.4 |

| FCFF | 51.3 | 44.8 | 59.3 | 78.6 |

| EPS | 2.97 | 2.97 | 3.26 | 5.6 |

| Price | 39.4 | 73.4 | 132.69 | 177 |

| Implied WACC | 7.5% | 4.4% | 4.2% | 3.5% |

Quelle: Zürcher Kantonalbank, Bloomberg

The decline in implied WACC however, cannot be fully explained by the strong fundamental performance. Part of the decline in the implied WACC can be alternatively explained by the benign monetary environment supported by declining interest rates (see chart) which fueled equity valuations. From a bottom-up perspective, it is interesting to note that, Apple’s Net-Debt position is actually negative – so essentially the company is debt free – and a decline in interest rates does not provide any real financial benefit to the company, except for an improving stock-valuation.

Interest rates & Implied WACC

What if we go back to a pre-Covid interest rate environment?

If we assume the bottom-up fundamental performance of Apple remains as strong as was in the past years, and consensus is right, then we can assess a potential share price downside if the prevailing interest environment goes back to the 2018/19 average. As we can see from the Table, all other things being equal, if we would start pricing a Pre-Covid interest rate environment, meaning a rise of the Cost of Capital (WACC) to 4.4%, the stock price would have a downside of approx. -27% (rel. to price at 31.12.2021). On the other side, based on previously paid financial multiples, the share price downside would be around 41%. These two approaches give us an indication about the possible valuation implications in a rising interest rate environment (see illustration below: if discount rates raise based on higher interest rates, valuation fall subsequently). If we combine both methodologies, we could consider a possible downside of -34% as reasonable. Clearly other factors like new successful product launches, margin expansions etc. could mitigate this negative impact.

| 2018-2019 Pre-Covid environment based on WACC | 2018-2019 Pre-Covid environment based on Multiple | Average based on both methodology | |

| Price 31.12.2021 | 177.6 | 177.6 | 177.6 |

| Fair Value | 130.0 | 104.0 | 117.0 |

| Downside | -26.8% | -41% | -34% |

Quelle: Zürcher Kantonalbank, Bloomberg

Link between valuations and rising interest rates

How can investors consider the risk of rising interest rates within an Equity Portfolio?

The Apple example is true for any stock that benefited from extremely loose monetary conditions, especially over the past three years. Taking that risk into account is possible by putting stock-valuations at the forefront of your investment process. Stocks with attractive valuations and a solid business model should benefit in this market environment.

Ultimately, like the environment of declining rates has pushed stocks well above their fundamental fair-value, the same process could be at work in the other direction. Stocks could be pushed below their fundamental fair values and this could create large opportunities for stock-pickers with a solid and disciplined stock selection process.