On the brink of stagflation

High inflation and a subdued economic outlook are pushing many economies towards the brink of stagflation. What does this mean for equity investments?

Text: Manuel Renz and Rocchino Contangelo

It is a consequence of the coronavirus crisis in combination with the low interest rate environment. Many major stimulus programmes were launched during the coronavirus crisis. The flood of money has come up against a tight supply situation since the spring of 2021. A very persistent effect of the coronavirus crisis is disrupted supply chains and logistics problems in international trade. Repeated lockdowns have not helped to alleviate this problem – on the contrary. The fact is that since the second quarter of 2021, prices have been increasing tremendously. This called the central banks into action at the beginning of 2022. Since then, they have turned their backs on their ultra-expansionary monetary policy. With drastic consequences for the valuation of investments.

The Russia-Ukraine conflict has exacerbated the price trends triggered by the coronavirus crisis. Russia and Ukraine are major producers/suppliers of oil and gas, metals, grain and fertilisers. The conflict and the associated sanctions against Russia are leading to supply shortages on the world markets and, while demand remains constant, to further price increases. The price increase was worsened in particular by the high dependence of European countries on Russian oil and gas supplies. Price increases in energy sources such as oil and gas have a strong inflationary effect because energy accounts for a large share of the basket on which inflation is calculated. With inflation rates of 9.1 % in the USA and an estimated 8.6 % in the euro area, one component of stagflation has already occurred.

What about economic development?

High prices are increasingly unsettling consumers. Price declines on the financial markets and high volatility are destroying assets. Economic research institutes are therefore unanimously reducing their economic outlooks.

When can we definitively say that we have stagnation? Intuitively, this is the case with zero growth. Many market players, however, define a stagnating economy as global economic growth of between 0 % and 2 %.

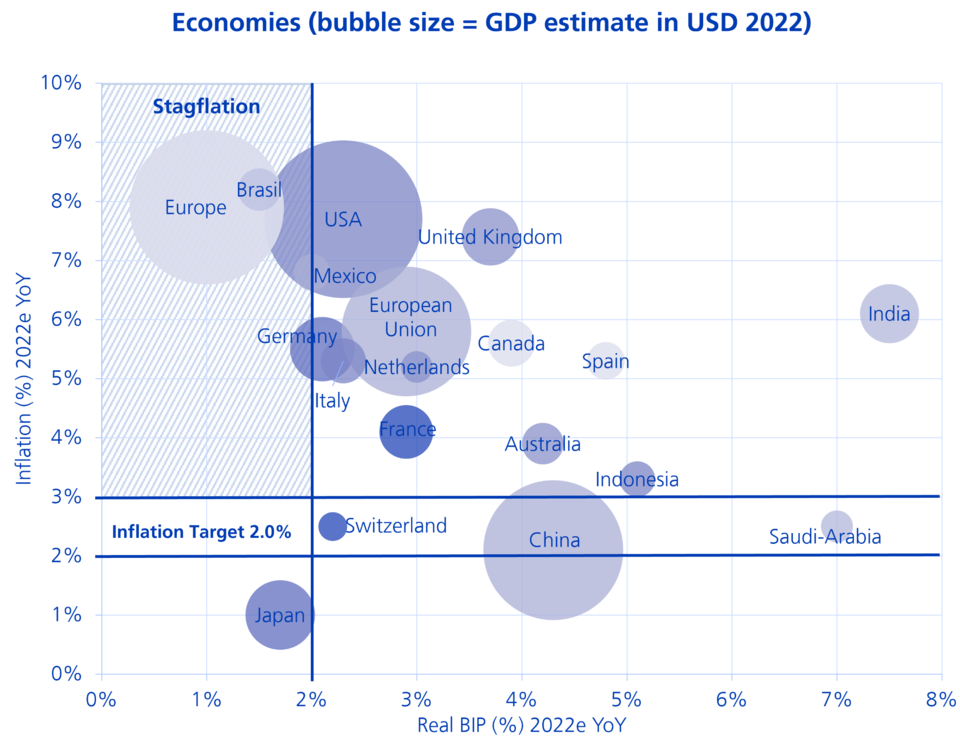

Current state of the 20 largest economies – risk of stagflation!

Many economies are already on the brink of stagflation. The chart below shows how we assess the 20 largest economies in terms of the risk of stagflation. A "stagflation corridor" has been determined for this purpose. This starts with real GDP growth of less than 2.0 % and simultaneous inflation of more than 3.0 % compared to the previous year (blue-shaded area). Accordingly, there is already a risk of stagflation for Europe as a whole and for Brazil. This is imminent for Mexico, Germany, Italy and the USA.

If the economic outlook continues to deteriorate, these economies will enter stagflation. Economies with a lower risk of stagflation are: Japan, Switzerland, China, Australia, Indonesia and Saudi Arabia. Switzerland is benefiting from low inflation compared to other economies due to the strength of the franc.

Global equity portfolio solutions in a stagflationary environment

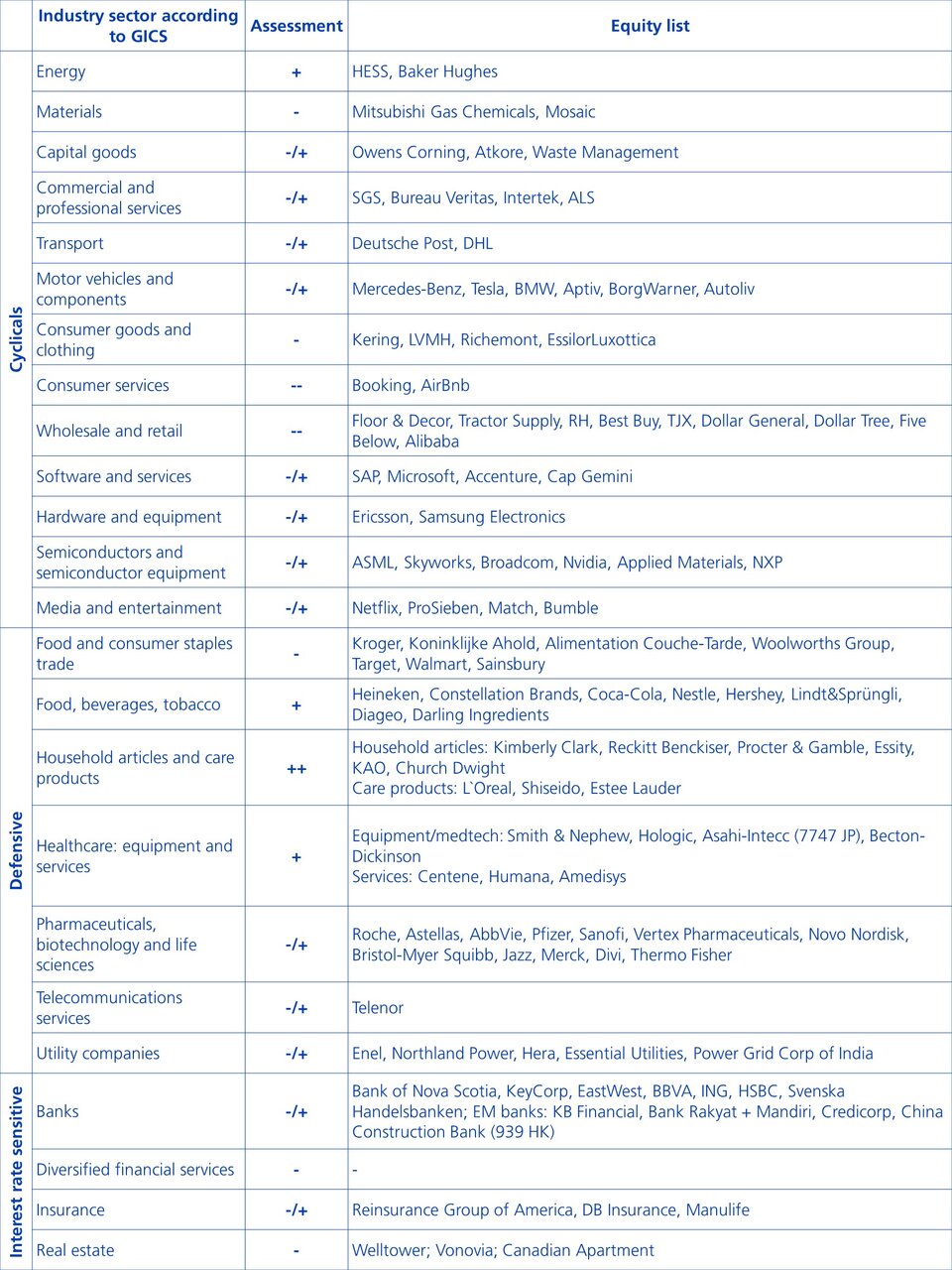

In addition to equity portfolio exposure to markets with lower stagflation risk, investors can also select sectors that historically outperform the benchmark in both a recessive and stagflationary environment.

In terms of cyclical stocks, only the energy sector can benefit from a stagflationary environment from a global perspective. The reasons for this are the strong demand and the low supply on the energy side. Investors are more likely to find what they are looking for in defensive stocks. In particular, the household articles and personal care products, food and beverages as well as healthcare (equipment and services) sectors. These sectors increasingly offer products that are always in demand regardless of the economic situation. The picture is rather mixed in the area of interest rate-sensitive stocks, e.g. banks and insurance companies. Although banks benefit from an increase in interest rates, there is also a high level of sensitivity to the financial market.

Heatmap for a stagflation scenario

At present, many economies are still in a good economic environment, supported by robust consumer behaviour and a strong labour market. Nevertheless, a more defensive positioning in a global equity portfolio is worthwhile in times of economic uncertainty. The sectors and equity securities shown serve as initial points of reference. Further fundamental analysis based on the securities is recommended. The focus should be on profitable and free cash flow (FCF)-generating companies that earn their cost of capital even in economically uncertain times. Companies, which do not have an urgent need for refinancing and are able to bear their debt burden. Another focus could be on favouring companies that benefit from structural and/or sustainably oriented profitable growth.

Legal notice: The publications were prepared by the Buy-Side Research of the Asset Management of Zürcher Kantonalbank. The information contained in this document has not been prepared in accordance with any legislation promoting the independence of financial research, nor is it subject to any prohibition on trading following the dissemination of financial research.