Green Bonds: Greenium decline in the CHF market

Our statistical analysis shows: The average yield differential between a green bond and a conventional bond (Greenium) in the CHF bond market has narrowed significantly over time. What this means for issuers and investors.

Author: Dr. oec. Jan Serwart, Portfolio Manager Fixed Income

The absolute and relative number of green bonds in the Swiss market (SBI AAA-BBB) has been steadily increasing for years. Of the total of 1,781 bonds (May 2024) in the Swiss Bond Index (SBI), 122 were green bonds. Their volume amounts to CHF 23.4 billion. This corresponds to a share of 4.4% of the total volume of the SBI.

What are green bonds?

Green bonds are bonds with which issuers exclusively finance projects that protect or reduce the burden on the environment. Examples of such projects include climate neutrality, electromobility, investments in energy-efficient technologies and circular economy projects. The structure and risk profile of a green bond are similar to those of a conventional bond from the same issuer, as are the expected returns.

Breakdown of Swiss green bonds by sector

The chart below shows the green bond breakdown for the Swiss Bond Index (SBI) as at May 2024 for various sectors. The financial sector (banks and insurance companies) currently has the highest number of outstanding green bonds at 56, while the Swiss Confederation currently has one.

Sector |

Number of green bonds |

Number of bonds in the sector |

Share (in %) of green bonds |

Finance (banks, insurance companies) |

56 |

392 |

14 |

Cantons, cities |

24 |

431 |

6 |

Supply (power stations, hospitals) |

12 |

101 |

12 |

Supranational |

10 |

44 |

23 |

Industry |

8 |

223 |

4 |

State agencies |

7 |

114 |

6 |

Mortgage-backed bonds |

4 |

410 |

1 |

State |

1 |

22 |

5 |

Other |

0 |

44 |

0 |

Total SBI AAA-BBB |

122 |

1'781 |

7 |

Development of greenium since 2021

Due to the high demand and low supply of green bonds, it became apparent at the beginning of the 2020ies that they often traded at a premium to a conventional bond with the same maturity. The difference in yield between the lower yields of green bonds compared to the higher yields of conventional bonds became known was named greenium.

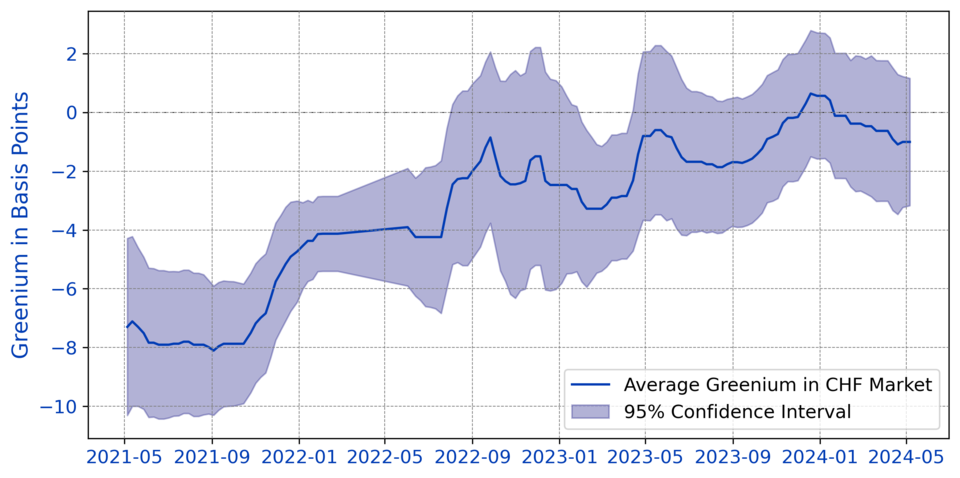

To date, few statistical statements have been made on the development of greenium in the Swiss bond market. We have now set ourselves this task. The basis for this was a comparison of the price development of green bonds and conventional bonds from the SBI's financial sector. The financial sector of the SBI is well suited for such a statistical analysis, because it has historically counted the most green bonds and the total number of bonds is large enough to be able to statistically estimate the average greenium in the CHF bond market.

The result shows: Greenium in the Swiss market has been trending downwards for three years.

How do we estimate the Greenium for the CHF bond market?

Each week, we estimate the greenium using a panel regression by regressing the spreads (interest rate premium on the risk-free swap interest rate) of the bonds on various control variables and a green bond indicator. The estimated coefficient of the green bond indicator reflects the average greenium in the market in the respective week. We control for maturity, squared maturity, rating, squared rating, payment rank, domestic dummy, emerging country dummy, callable dummy, HQLA level and Bloomberg ticker dummies at issuer level.

In mid-2021, the average greenium was between six and eight basis points. The average greenium fell continuously to around one basis point by September 2022. Statistically speaking, since then it has no longer been possible to determine with 95% certainty whether there is a general greenium in the Swiss bond market or not. This can be seen graphically when the blue-coloured confidence inverval exceeds the zero line (no greenium). In individual cases, there are still green bonds with an average greenium of between zero and two basis points.

Causes of the decline in greenium

The decline in the greenium in recent years can be attributed to the following factors: On the one hand, sustainability funds with green quotas or comparable requirements created a high, simultaneous buying demand from many investors. These quotas have been met over time, resulting in a decline in the simultaneous demand for green bonds. On the other hand, the supply of green bonds is steadily increasing as more and more issuers are switching to sustainable financing. This increase in supply coupled with a decline in demand led to a decrease in the greenium for green bonds.

What nevertheless speaks in favour of green bonds

The existence of a greenium makes it attractive for issuers to issue green bonds, as they have to pay less of a spread premium (interest). The decline in the greenium means that the economic attractiveness for organisations to issue green bonds has decreased. Nevertheless, there are still numerous reasons why it still makes sense to issue green bonds, which is reflected by the fact that the number of green bonds in the SBI is still increasing.

The reasons:

- A broader investor base can be reached by issuing green bonds, as more and more investors are showing interest in sustainable investments.

- Larger financing amounts are often possible, as green bonds can be bought by a broader range of financial vehicles of institutional investors. In addition, in individual cases there may still be a greenium that averages between zero and two basis points.

- Positive external impact: Issuing green bonds sends a positive message to the outside world and signals a strong commitment to sustainability.

From an investor's point of view, the greenium reduction is an advantage, as they can now buy green bonds without having to sacrifice returns significantly. This makes them all the more attractive for investors, as they are interesting from a climate perspective and yet do not mean a loss of yield. For our own funds, we track the development of the greenium and make it part of our investment decisions.