Artificial intelligence: unlocking hidden sources of alpha

The financial sector is one of the sectors of the global economy with the highest availability of data. How can this huge amount of data be used cleverly? Can this help generate an excess return in the equities sector?

Stefan Fröhlich

The digital age has given rise to mountains of data. The International Data Corporation estimates that the world generates more data every two days than all humanity throughout history up to 2003. More than 10,000 reports, news and social media stories for international companies are published daily on the financial services platform Bloomberg. This big data revolution creates new opportunities, especially in the financial industry.

Traditionally, financial market data is assessed by analysts and fund managers and investment decisions are made based on human intuition. However, given the exponentially growing amount of data, it is becoming increasingly difficult to extract the really important information from the

flood of data and identify the drivers of returns that can be used to estimate future price developments. Big data technologies have great potential in the financial sector, as computer algorithms are ideal for processing huge volumes of data and detecting patterns in data sets at high speed.

Deriving insights from data

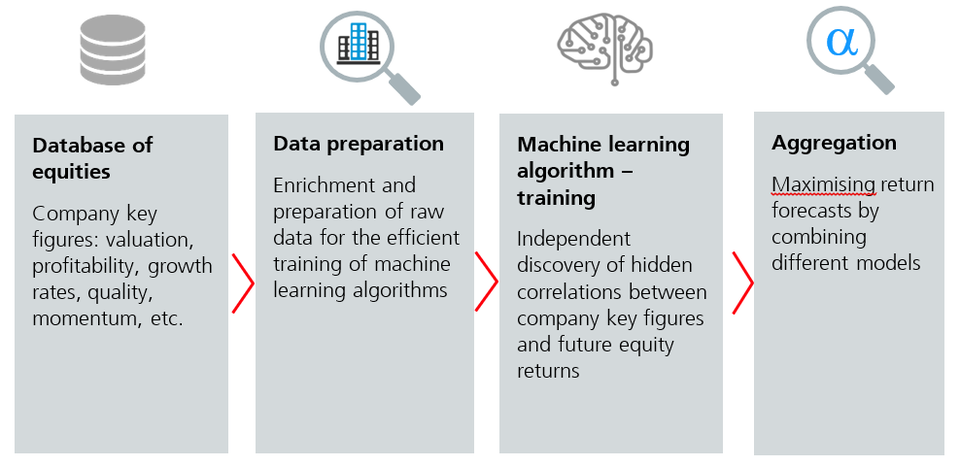

State-of-the-art machine learning algorithms are able to independently scour financial market data and uncover hidden correlations between business metrics and future returns without human assistance. This process can be divided into four steps:

- Database of equities

The basis for all machine learning algorithms is an extensive database covering decades of history for all equities worldwide and all available company data (valuation, profitability, growth, analyst estimates, risk indicators, momentum, etc.). The more data the learning algorithm has available for training, the better and more stable the achieved return forecasts will be. - Data preparation

In order for the algorithms to be able to learn efficiently, the raw data is generally enriched and further prepared with supplementary key figures. This can be done, for example, by transforming or neutralising the data. - Training of machine learning algorithms

In this step, the algorithm learns independently from the prepared data. It analyses which combination of company key figures leads to above-average returns and determines the characteristics of equities with poor performance. Based on these findings, the algorithm then automatically derives complex models that can be used to estimate future price developments for all equities worldwide. These comprehensive forecasts are hardly possible for humans, as a large number of analysts would be needed to make daily return forecasts for thousands of equities. - Aggregation

To further increase the probability of return forecasts materialising, different types of algorithms are combined. In this way, models can be linked that are specialised in short-term (tactical) and long-term (strategic) forecasts or have their strength in upwards or downwards trending markets. Dynamic aggregation of different prediction models leads to more stable and reliable forecasts.

Artificial intelligence – innovative technology for financial investments

Equity strategies based on machine learning algorithms tap into sources of alpha that were previously hidden from humans due to their high complexity.

These strategies adapt quickly and dynamically to changing market conditions and can generate additional returns even in difficult phases – such as the IT bubble, the financial crisis or the coronavirus pandemic. The excess returns determined in back-testing are promising and also only slightly correlated with the returns of traditional equity funds that pursue a fundamental approach. Compared to systematic investment strategies, which usually have permanent style orientations such as value or quality, strategies based on machine learning do not have permanent style bets.

So far, there are few publicly available equity products that use machine learning algorithms for stock selection. An investment solution will be added in autumn 2021: Swisscanto will issue artificial intelligence equity certificates for the first time, the selection process of which is based entirely on artificial intelligence. With this innovation, access to previously hidden sources of alpha is open to all investors.